Introduction

You do not need to be an accountant to understand your business numbers.

Many Edmonton small business owners avoid looking at their books because the reports feel confusing. Profit and loss, balance sheet, accounts receivable, accounts payable, GST/HST payable, shareholder loan, bank reconciliation, payroll liabilities — it can feel like a different language.

But here is the truth: you do not need to understand every accounting rule to read your books properly.

You only need to know what to look for.

Your books are not just for your accountant or tax preparer. They are a practical tool that can help you answer important business questions:

Am I actually making money?

Where is my cash going?

Which customers still owe me?

Are my expenses getting too high?

Can I afford payroll, rent, tax, or new equipment?

Do I have enough set aside for GST/HST?

Are my books clean enough for tax time?

For Edmonton business owners, clean bookkeeping is not just about compliance. It helps with cash flow, pricing, hiring, planning, and decision-making. Whether you run a construction company, restaurant, retail store, consulting business, trucking business, ecommerce store, clinic, or professional service company, understanding your books can help you run the business with more confidence.

This guide explains how to read your books without being an accountant.

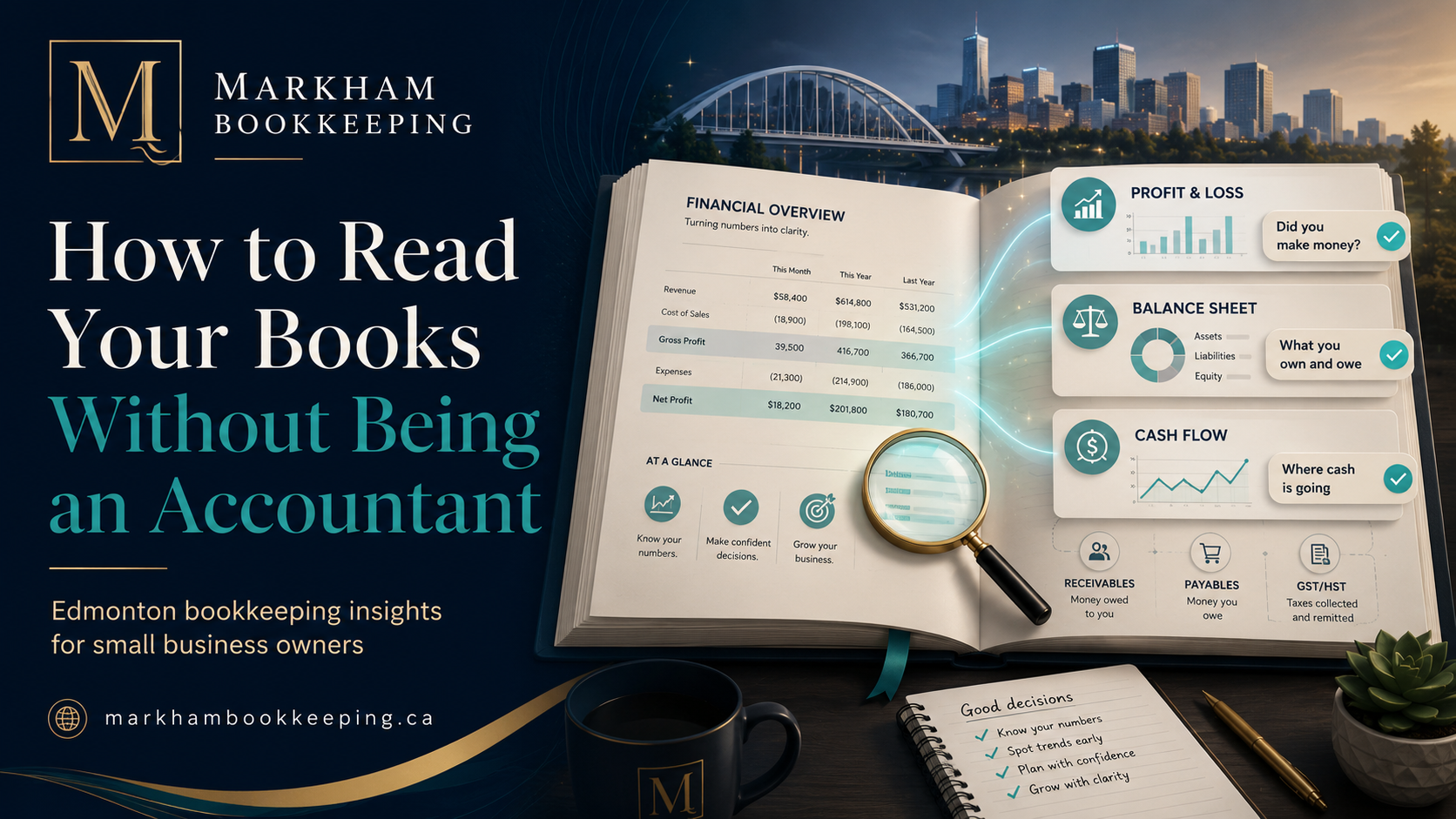

Start With the Profit and Loss Report

The first report most small business owners should learn to read is the Profit and Loss report, also called the income statement.

This report shows:

Income minus expenses equals profit or loss.

In simple terms, it tells you whether the business made money during a specific period.

For example, you can run a profit and loss report for one month, one quarter, or one full year. If you are using QuickBooks, Xero, Sage, or another accounting software, this report is usually easy to generate.

Your profit and loss report usually has three main sections:

Income

Cost of goods sold, if applicable

Expenses

Income means sales or revenue. This is the money your business earned from customers.

Cost of goods sold means direct costs related to producing or delivering your product or service. For example, materials, subcontractors, product purchases, shipping, packaging, or direct labour may fall into this area depending on your business.

Expenses are operating costs such as rent, software, insurance, bookkeeping, payroll, meals, advertising, vehicle expenses, bank fees, phone bills, and office supplies.

The key question is simple:

After paying the business expenses, is there anything left?

If your profit and loss report shows sales of $80,000 and expenses of $72,000, your profit is $8,000. That does not automatically mean you have $8,000 sitting in the bank, but it does mean the business made a profit on paper.

Profit Is Not the Same as Cash

This is one of the most important things to understand.

A business can show profit but still have low cash.

Why?

Because profit and cash are different.

You may have profit because you invoiced customers, but those customers have not paid yet. You may have used cash to pay down a loan, buy equipment, pay old bills, or pay yourself through draws. Those payments may not all appear as regular expenses on the profit and loss report.

For example, if your Edmonton business made $15,000 in profit but used $12,000 to pay down a business loan, your bank account may not feel strong even though the business was profitable.

That is why you should not rely only on the profit and loss report.

You also need to look at your balance sheet and cash flow.

Check the Balance Sheet

The balance sheet shows what your business owns, what it owes, and what is left for the owner.

It is usually broken into three parts:

Assets

Liabilities

Equity

Assets are things the business owns or controls. This can include bank accounts, accounts receivable, inventory, equipment, vehicles, prepaid expenses, and deposits.

Liabilities are amounts the business owes. This can include credit cards, loans, accounts payable, GST/HST payable, payroll liabilities, corporate tax payable, and other debts.

Equity is the owner’s interest in the business. For corporations, this may include retained earnings and shareholder loans.

The balance sheet answers questions like:

How much cash is in the bank?

How much do customers owe?

How much do I owe suppliers?

How much GST/HST is payable?

How much debt is on the books?

Are shareholder loans recorded correctly?

Does the business look financially stable?

You do not need to understand every account. Start by reviewing the big numbers.

If your bank balance looks wrong, your books may not be reconciled.

If accounts receivable is high, customers may not be paying on time.

If accounts payable is high, bills may be piling up.

If GST/HST payable is high, you may need to set aside cash before the filing deadline.

If shareholder loan looks strange, owner payments or personal expenses may need review.

The balance sheet is often where messy bookkeeping becomes obvious.

Review the Bank Balance Carefully

One of the easiest ways to read your books is to compare your accounting software bank balance to your actual bank statement.

If your bank account in QuickBooks or Xero says $25,000 but your actual bank statement says $18,000, something is wrong or unreconciled.

This is why bank reconciliation matters.

A clean bank reconciliation confirms that the transactions in your bookkeeping system match what actually happened in the bank.

For Edmonton small businesses, this should usually be done monthly.

When the bank is not reconciled, your reports may not be reliable. You could have duplicate expenses, missing deposits, old transactions, incorrect transfers, or payments posted to the wrong account.

Before trusting any report, ask:

Are the bank and credit card accounts reconciled?

If the answer is no, be careful. The numbers may not be ready for decision-making.

Look at Accounts Receivable

Accounts receivable means money customers owe your business.

If you send invoices to customers, this report is very important.

The accounts receivable report tells you:

Who owes you money

How much they owe

How long the invoice has been unpaid

A healthy business does not just make sales. It collects the money.

For example, your profit and loss report may show $60,000 in sales for the month. But if $25,000 of those invoices are still unpaid, your cash flow may be tight.

This is common for contractors, consultants, professional services, and B2B businesses in Edmonton.

When reading your accounts receivable, pay attention to old invoices. If an invoice is more than 30, 60, or 90 days overdue, it may create cash flow problems.

Ask yourself:

Are customers paying on time?

Are old invoices still sitting unpaid?

Were payments received but not matched properly?

Do I need to follow up with customers?

Accounts receivable is one of the fastest ways to understand why a profitable business may still feel short on cash.

Look at Accounts Payable

Accounts payable means bills your business owes to suppliers, vendors, contractors, or service providers.

This report helps you understand upcoming cash pressure.

If accounts payable is high, you may have a lot of bills due soon. Even if your bank balance looks good today, upcoming payments may reduce your cash quickly.

For example, your business may have $20,000 in the bank, but if you owe $18,000 to suppliers, your available cash is not really $20,000.

Accounts payable is especially important for businesses with supplier accounts, construction materials, inventory purchases, subcontractors, rent, utilities, and professional fees.

When reading this report, ask:

Which bills are due soon?

Are any bills overdue?

Were bills paid but not marked as paid?

Are duplicate bills sitting in the system?

Do I have enough cash to cover upcoming payments?

Clean accounts payable helps you avoid surprises.

Watch Your Biggest Expenses

You do not need to review every tiny transaction to understand your books.

Start with the biggest expense categories.

Look at your profit and loss report and ask:

What are my top five expenses?

Are any expenses higher than expected?

Did payroll increase?

Did advertising increase?

Did vehicle expenses increase?

Are meals, travel, subscriptions, or software costs getting out of control?

Are personal expenses mixed into the business?

For many Edmonton small businesses, common major expenses include payroll, rent, subcontractors, materials, fuel, insurance, advertising, software, professional fees, and vehicle costs.

The goal is not to cut every expense. The goal is to understand where the money is going.

A business owner who knows their biggest costs can make better decisions about pricing, budgeting, hiring, and cash flow.

Understand GST/HST Payable

If your business is registered for GST/HST, your books should help you understand how much tax you may owe.

GST/HST payable is usually shown on the balance sheet as a liability.

This amount represents sales tax collected from customers, reduced by eligible input tax credits, depending on your filing method and transaction coding.

You do not need to calculate the full return manually every time, but you should understand the basic idea:

GST/HST collected is not your money.

It belongs to the government and should be tracked separately.

If your books show a GST/HST payable balance, make sure you have cash available to pay it when the filing deadline comes.

A common mistake is treating all bank deposits as available cash. But if part of that money includes GST/HST collected, spending it can create trouble later.

For Edmonton businesses that file GST/HST quarterly or annually, this is very important. Good bookkeeping helps you avoid a surprise tax bill.

Review Payroll Liabilities

If you have employees, payroll liabilities matter.

Payroll liabilities may include amounts withheld or owed for income tax, CPP, EI, and other payroll-related items.

These amounts should not be ignored because payroll remittances have deadlines.

If payroll entries are missing or posted incorrectly, your books may understate what the business owes.

When reading your books, check whether payroll liabilities make sense. If the balance keeps growing and remittances are not being recorded properly, there may be an issue.

For Edmonton employers, payroll bookkeeping should be accurate because payroll errors can create penalties, employee issues, and year-end T4 problems.

Compare This Month to Last Month

One of the easiest ways to read your books is to compare periods.

Instead of looking at one report in isolation, compare:

This month vs last month

This quarter vs last quarter

This year vs last year

This helps you spot trends.

For example:

Sales increased, but profit decreased.

Payroll increased faster than revenue.

Advertising spending went up, but sales did not.

Bank fees increased.

Vehicle expenses doubled.

Accounts receivable is growing.

Cash is lower even though income is higher.

These trends tell a story.

You do not need to be an accountant to ask practical questions. If something looks unusual, investigate it.

Good bookkeeping makes these comparisons easier because the numbers are organized consistently.

Watch for Red Flags in Your Books

When reading your books, look for warning signs.

Common red flags include:

Bank accounts are not reconciled.

Negative balances appear where they should not.

Old unpaid invoices are still sitting.

Old unpaid bills are still sitting.

Expenses are posted to “Ask My Accountant” or “Uncategorized Expense.”

Transfers are recorded as income.

Credit card payments are recorded as expenses.

Loan payments are recorded fully as expenses.

GST/HST payable does not make sense.

Payroll liabilities are not clearing.

Shareholder loan keeps changing without explanation.

Large transactions have no receipts.

These issues do not always mean something serious is wrong, but they do mean the books need review.

Clean books should tell a clear story. Messy books create confusion.

Build a Simple Monthly Review Routine

You do not need to spend hours reading reports.

A simple monthly review can make a big difference.

Start with these steps:

Review the profit and loss report.

Check the bank and credit card reconciliations.

Review accounts receivable.

Review accounts payable.

Check GST/HST payable.

Review payroll liabilities, if applicable.

Look at the largest expenses.

Compare current month to previous month.

Ask questions about anything unusual.

This monthly habit helps Edmonton small business owners stay ahead of problems instead of discovering everything at year-end.

It also makes conversations with your bookkeeper or accountant easier because you know what you are looking at.

How a Bookkeeper Helps You Understand Your Books

A good bookkeeper does more than enter transactions.

A bookkeeper helps organize your financial records so the reports are useful.

For example, an Edmonton bookkeeper can help with:

Bank reconciliation

Credit card reconciliation

Expense categorization

Receipt organization

Accounts receivable tracking

Accounts payable tracking

GST/HST tracking

Payroll bookkeeping

Monthly financial reports

Bookkeeping cleanup

Year-end preparation

When the books are clean, business owners can read the reports more easily.

Instead of guessing, you can make decisions based on real numbers.

Final Thoughts

You do not need to be an accountant to read your books.

You need clean records, basic financial awareness, and a simple monthly review process.

Start with the profit and loss report to understand income and expenses. Review the balance sheet to understand what the business owns and owes. Check accounts receivable to see who owes you money. Check accounts payable to see what bills are coming. Review GST/HST and payroll liabilities so tax deadlines do not surprise you. Compare results month to month so you can spot trends early.

For Edmonton small business owners, reading your books is not about becoming an accounting expert. It is about understanding your business well enough to make better decisions.

Clean books help you see what is really happening.

At Markham Bookkeeping, we help Edmonton small businesses keep their books organized, accurate, and easier to understand.

Need help reading your books or cleaning up your bookkeeping in Edmonton? Markham Bookkeeping can help you get clear, reliable numbers.

FAQ

1. Do I need to be an accountant to understand my books?

No. You do not need to know every accounting rule. You only need to understand the main reports, such as profit and loss, balance sheet, accounts receivable, accounts payable, GST/HST payable, and bank reconciliation.

2. What is the most important report for small business owners?

The profit and loss report is usually the best place to start because it shows income, expenses, and profit. However, you should also review the balance sheet and cash flow-related reports.

3. Why does my business show profit but have no cash?

Profit and cash are different. Your money may be tied up in unpaid invoices, loan payments, equipment purchases, owner draws, inventory, or tax payments.

4. How often should I review my books?

Most small business owners should review their books monthly. High-volume businesses may benefit from weekly reviews.

5. What does it mean if my bank balance does not match my bookkeeping?

It usually means the account is not reconciled or there are missing, duplicate, or incorrectly recorded transactions. Bank reconciliation should be completed before relying on reports.

6. Can a bookkeeper help explain my reports?

Yes. A bookkeeper can help organize your records, reconcile accounts, prepare monthly reports, and explain what the numbers mean in practical terms.