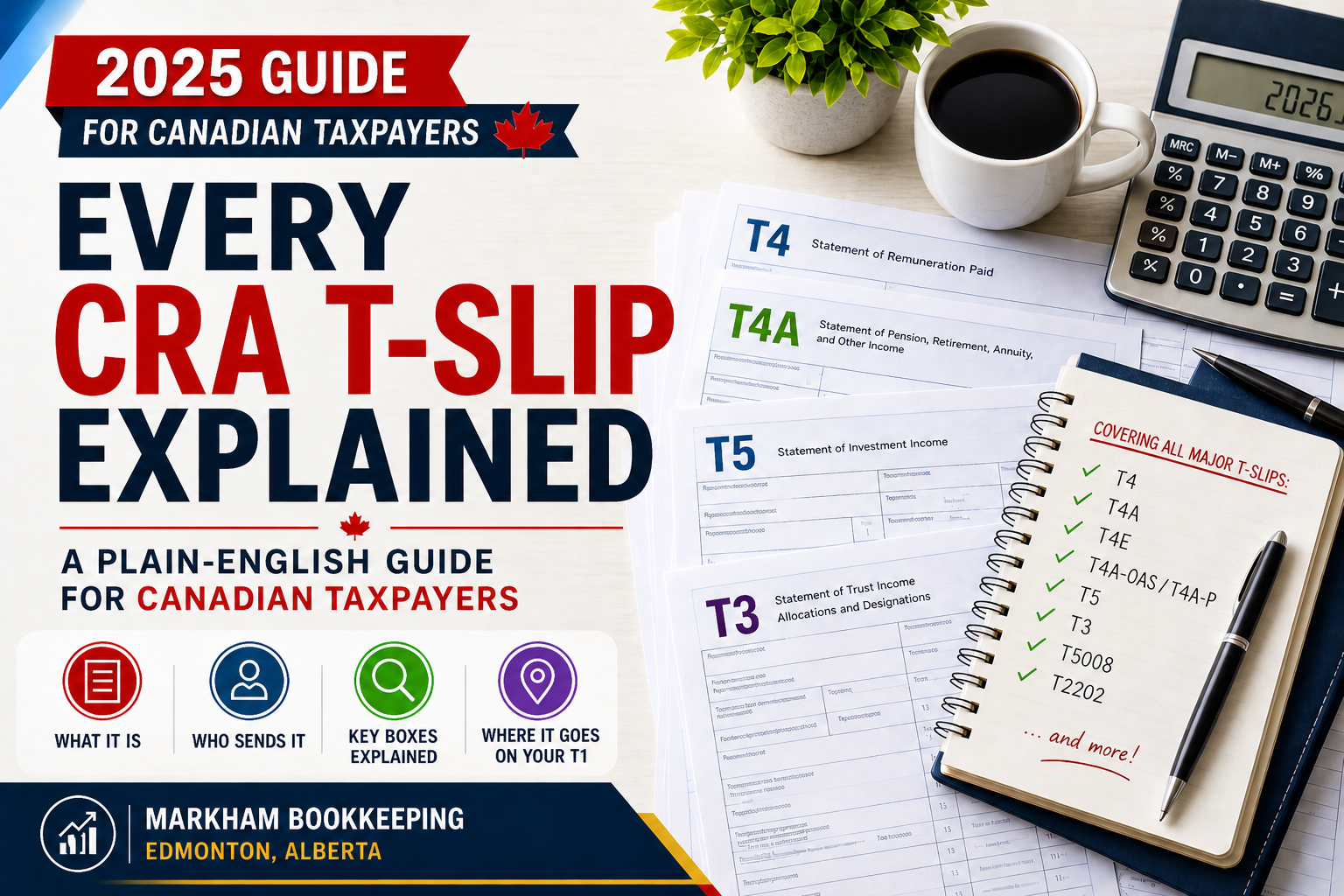

Tax season rolls around every year, and every year I hear the same thing from clients: “I got this slip in the mail and I have no idea what to do with it.”

If that sounds familiar, you are not alone. The Canada Revenue Agency issues over a dozen different T-slips, each tied to a different type of income or benefit. Some people get one. Some people get six. And if you are a newcomer to Canada, a gig economy worker, or a retiree, the pile can feel genuinely overwhelming.

This guide breaks down every major CRA T-slip in plain English — what it is, who sends it to you, what the key boxes mean, and where it goes on your T1 personal tax return. Bookmark this page. You will need it again next February.

First: How to Stay Organized Before You File

Before we get into each slip, here is what I tell every client at the start of tax season:

Do not file until you have every slip in hand. CRA cross-references what you report against what your employers, banks, and government agencies have already submitted. If there is a mismatch, you will get a letter — and nobody wants a CRA letter.

The best way to confirm you have everything is to log into CRA My Account at canada.ca and check the “Tax information slips” section. By late February or early March, most slips are already uploaded there. If a slip is missing from your mailbox, My Account is your first stop.

Now, let’s go through each one.

T4 — Statement of Remuneration Paid

Who sends it: Your employer.

What it covers: Employment income — your salary, wages, tips reported through payroll, bonuses, and taxable benefits like a company car or employer-paid premiums.

Key boxes to know:

- Box 14 — Employment income. This is your gross pay before deductions.

- Box 22 — Income tax deducted. What your employer withheld on your behalf.

- Box 16 — CPP contributions.

- Box 18 — EI premiums.

- Box 40 — Taxable benefits (like a group life insurance premium your employer paid).

- Box 52 — Pension adjustment. Reduces your RRSP room if you have a workplace pension.

Where it goes on your T1: Employment income on Line 10100. The deductions in Boxes 16, 18, and 22 flow into credits and deductions sections.

Common issues: If you worked multiple jobs, you get a T4 from each employer. Make sure you have all of them. If an employer went out of business mid-year, CRA My Account is your backup.

T4A — Statement of Pension, Retirement, Annuity, and Other Income

Who sends it: A wide range of payers — employers paying severance, pension plan administrators, insurance companies paying out annuities, and the government for certain benefits.

What it covers: This is the catch-all slip. If you received self-employment fees reported through a corporation or institution, scholarships, fellowships, research grants, RESP educational assistance payments, or payments from a registered pension plan that is not CPP or OAS — it lands on a T4A.

Key boxes to know:

- Box 016 — Pension or superannuation income.

- Box 020 — Self-employment commissions. Contractors paid by corporations often receive this.

- Box 028 — Other income. Read this carefully — it covers a lot.

- Box 105 — Scholarships and bursaries. Generally tax-exempt for full-time students.

- Box 130 — RESP educational assistance payments.

Where it goes on your T1: Depends on the box. Box 016 goes to Line 11500. Box 020 is self-employment income reported on a T2125. Box 105 may be tax-exempt.

Common issues: Many contractors are surprised to receive a T4A instead of a T4. If you did work as an independent contractor for a single client who paid you through their payroll system, you may see Box 020. Do not ignore it — CRA sees it.

T4E — Statement of Employment Insurance and Other Benefits

Who sends it: Service Canada.

What it covers: EI benefits you received during the year, including regular EI, maternity and parental benefits, sickness benefits, and compassionate care benefits.

Key boxes to know:

- Box 14 — Total benefits paid.

- Box 15 — Regular EI benefits.

- Box 16 — Maternity/parental benefits.

- Box 26 — Income tax deducted.

Where it goes on your T1: Line 11900.

Common issues: EI is taxable income. Many people on mat leave are surprised when they owe taxes in April. If your family income is high, a portion of EI may be clawed back under the repayment rules — Box 30 on the T4E flags this.

T4A-OAS — Statement of Old Age Security

Who sends it: Service Canada.

What it covers: Old Age Security pension payments you received during the year.

Key boxes to know:

- Box 18 — Gross OAS pension paid.

- Box 22 — Income tax withheld.

- Box 21 — OAS repaid (if your net income triggered a clawback).

Where it goes on your T1: Line 11300. If you had a clawback (the OAS recovery tax), that gets reported separately.

Common issues: OAS starts being clawed back once your net income exceeds roughly $90,997 (2024 threshold — confirm annually). If you are near that range, proactive RRSP contributions earlier in the year can help reduce the hit.

T4A-P — Statement of Canada Pension Plan Benefits

Who sends it: Service Canada.

What it covers: CPP retirement, disability, or survivor benefits you received.

Key boxes to know:

- Box 14 — CPP retirement pension.

- Box 16 — CPP disability benefits.

- Box 20 — CPP death benefit (lump sum, reported differently).

Where it goes on your T1: Line 11400 for retirement benefits.

Common issues: CPP disability benefits may qualify for the disability tax credit depending on your situation. Do not just drop the number on Line 11400 without checking eligibility for related credits.

T4PS — Statement of Employees Profit-Sharing Plan Allocations and Payments

Who sends it: Your employer, if your workplace has a profit-sharing plan.

What it covers: Amounts allocated to you under an employees’ profit-sharing plan (EPSP), which may include cash payments, shares, or other property.

Where it goes on your T1: Depends on the type of allocation — can flow as employment income or investment income depending on what was distributed.

Common issues: EPSPs involving employer contributions can trigger EPSP tax in some structures. Not common, but if you receive this slip, read it carefully or have a bookkeeper review it.

T4RSP — Statement of RRSP Income

Who sends it: Your financial institution.

What it covers: Withdrawals you made from your RRSP during the year. Also used for Home Buyers’ Plan and Lifelong Learning Plan repayments and withdrawals.

Key boxes to know:

- Box 22 — RRSP income (straight withdrawals).

- Box 27 — HBP withdrawal amount.

- Box 25 — LLP withdrawal amount.

Where it goes on your T1: Line 12900 for regular withdrawals.

Common issues: RRSP withdrawals are fully taxable as income in the year they are taken. Withholding tax is applied at source, but it may not cover your full tax liability — especially if you are in a higher bracket. Plan withdrawals carefully.

T4RIF — Statement of Income from a Registered Retirement Income Fund

Who sends it: Your financial institution.

What it covers: Mandatory or voluntary withdrawals from your RRIF. Once you convert your RRSP to a RRIF (required by the end of the year you turn 71), you must withdraw a minimum amount annually.

Key boxes to know:

- Box 16 — Taxable amounts received.

- Box 24 — Excess amount (anything above the minimum).

Where it goes on your T1: Line 11500.

Common issues: The minimum RRIF withdrawal amount increases as you age. Only the excess above the minimum qualifies for pension income splitting with a spouse.

T5 — Statement of Investment Income

Who sends it: Your bank, credit union, brokerage, or any institution that paid you investment income.

What it covers: Interest income, eligible dividends, and non-eligible dividends earned from Canadian sources.

Key boxes to know:

- Box 13 — Interest from Canadian sources.

- Box 24 — Eligible dividends (from large public corporations).

- Box 25 — Dividend tax credit for eligible dividends.

- Box 10 — Non-eligible dividends (from small business corporations).

Where it goes on your T1: Interest on Line 12100. Dividends on Line 12000 (eligible) and Line 12010 (non-eligible). The gross-up and dividend tax credit mechanism applies automatically when you enter the amounts correctly.

Common issues: T5s are only issued if your investment income from a single institution exceeds $50 in the year. Below that threshold, no slip is issued — but the income is still taxable and still needs to be reported. Keep your own records.

T3 — Statement of Trust Income Allocations and Designations

Who sends it: A mutual fund trust, ETF trust, estate, or inter vivos trust.

What it covers: Income flowed out from a trust to you as a beneficiary — including interest, dividends, foreign income, and capital gains.

Key boxes to know:

- Box 21 — Capital gains.

- Box 23 — Actual amount of eligible dividends.

- Box 26 — Other income.

- Box 49 — Foreign income.

Where it goes on your T1: Scattered across multiple lines depending on income type. Capital gains go to Schedule 3. Dividends flow through the gross-up mechanism. Foreign income may generate a foreign tax credit.

Common issues: T3 slips are issued late — the deadline is 90 days after the trust’s year-end, which for calendar-year trusts is March 31. If you hold mutual funds or ETFs in a non-registered account, wait for your T3 before filing. Filing without it and needing to refile is a common and avoidable headache.

T2202 — Tuition and Enrolment Certificate

Who sends it: Your college, university, or designated educational institution.

What it covers: Eligible tuition fees paid and the months of full-time and part-time enrolment. This determines your tuition tax credit.

Key boxes to know:

- Box B — Eligible tuition fees.

- Box C / D — Months of full-time and part-time enrolment (affects the education and textbook amounts for prior years).

Where it goes on your T1: Schedule 11. Unused amounts can be carried forward indefinitely or transferred to a parent, grandparent, or spouse (up to $5,000).

Common issues: Students often forget to carry forward unused tuition credits year over year. If you graduated a few years ago and never fully used your credits, they are still sitting there on your CRA My Account.

T5007 — Statement of Benefits

Who sends it: Provincial social assistance programs, workers’ compensation boards, or welfare agencies.

What it covers: Social assistance payments and workers’ compensation benefits you received during the year.

Key boxes to know:

- Box 10 — Workers’ compensation benefits.

- Box 11 — Social assistance payments.

Where it goes on your T1: These amounts are reported as income on Lines 14400 and 14500, but here is the critical detail — they are not actually taxable. They get added to net income for the purpose of calculating income-tested benefits and credits (like the GST/HST credit and the Canada Child Benefit), then deducted again before taxable income is calculated.

Common issues: This confuses a lot of people. Clients sometimes see the T5007 amount on their return and panic that they owe tax on social assistance. You do not. It flows in and flows out — but it must be reported correctly or you risk losing benefit eligibility.

T5008 — Statement of Securities Transactions

Who sends it: Your broker or financial institution.

What it covers: Proceeds from the sale of securities — stocks, bonds, ETFs, options, and other investments sold through your brokerage account.

What it does NOT tell you: Your adjusted cost base (ACB). The T5008 shows proceeds only. You are responsible for tracking your ACB yourself.

Where it goes on your T1: Schedule 3 (Capital Gains). You calculate the gain or loss by subtracting your ACB and any selling costs from the proceeds.

Common issues: This is one of the most misunderstood slips. Getting a T5008 does not automatically mean you owe tax. If you sold at a loss, you have a capital loss. If you sold for a gain, only 50% of the gain is included in income (the inclusion rate — confirm for 2024 and 2025 given recent proposed changes). Keep your own ACB records.

T5013 — Statement of Partnership Income

Who sends it: A partnership you are a member of.

What it covers: Your share of partnership income, losses, deductions, and credits from a business operated as a partnership.

Where it goes on your T1: Depends on the type of income within the partnership — business income, investment income, capital gains, etc. each flow to their respective lines.

Common issues: Partnerships involving limited partners in tax shelters can be complex. If you are in a limited partnership investment, have a professional review the T5013 before filing.

RC62 — Universal Child Care Benefit Statement

Who sends it: CRA (for years prior to 2016, when UCCB was replaced by CCB).

Note: The Universal Child Care Benefit was eliminated in 2016 and replaced by the Canada Child Benefit (CCB). CCB is non-taxable and does not generate a slip. If you are seeing an RC62, it is for a prior-year reassessment. The CCB itself does not need to be reported on your return.

RC210 — Canada Workers Benefit Advance Payments Statement

Who sends it: CRA.

What it covers: Advance payments of the Canada Workers Benefit (CWB) that were issued to you during the year.

Where it goes on your T1: Schedule 6. The advance is reconciled against your actual CWB entitlement when you file. If you received more in advances than you were entitled to, you may owe some back.

Common issues: The CWB is an income-tested refundable tax credit for lower-income workers. Advance payments were introduced to get money in people’s hands faster. Make sure you report this slip — CRA will catch it if you do not.

What to Do If a Slip Is Missing or Wrong

Missing slip: Log into CRA My Account first. Most slips are there by early March. If a slip is genuinely not uploaded and you cannot reach the issuer, you can still file using your best estimate and note it as estimated — then adjust once the slip arrives.

Wrong slip: Contact the issuer to request an amended slip. They will file a corrected version with CRA. Do not just cross out numbers on the original — the amended slip needs to flow through the system.

Slip arrived after you filed: File a T1 adjustment (T1-ADJ) or through My Account to amend your return. Do not file a second return.

Final Thoughts

Tax slips are not designed to confuse you — but there are a lot of them, and each one has its quirks. The key is knowing which slips to expect based on your situation, waiting until you have all of them before filing, and understanding that receiving a slip does not always mean you owe more tax.

If you are an Edmonton small business owner, gig economy worker, newcomer, or retiree navigating multiple slips, Markham Bookkeeping can help. We prepare T1 personal returns, handle complex slip situations, and make sure you are claiming every credit you are entitled to.

Ready to file with confidence? Contact Markham Bookkeeping at markhambookkeeping.ca.