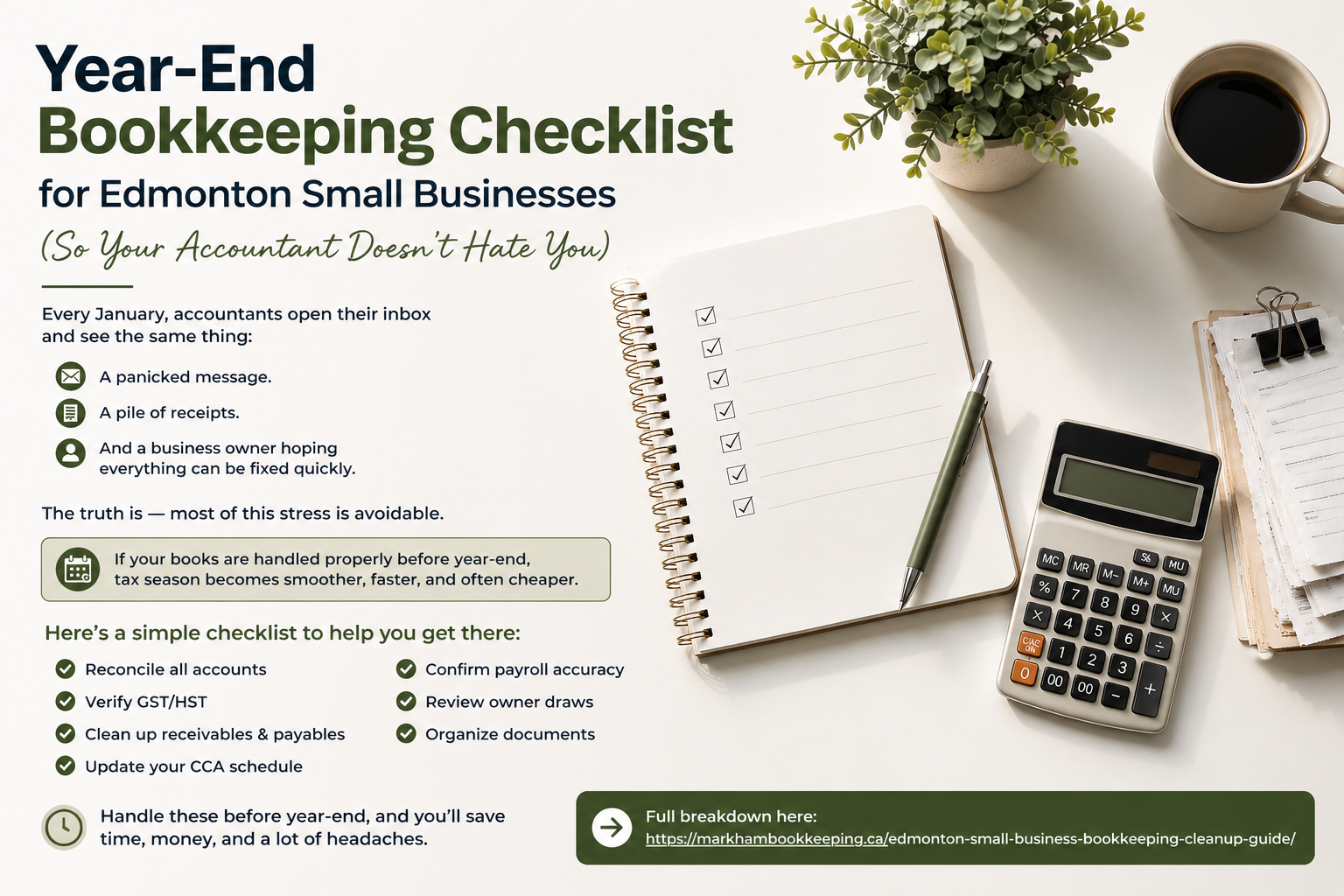

So Your Accountant Doesn’t Hate You

Every January, accountants across Edmonton open their inbox to the same thing:

A rushed email.

A stack of unorganized receipts.

And a business owner hoping everything can be fixed quickly.

If that sounds familiar, you’re not alone.

But here’s the reality — most of this stress is completely avoidable.

When your books are handled properly before year-end, tax season becomes smoother, faster, and often far less expensive. Instead of paying your accountant to fix errors, you’re paying them to help you save tax and make smarter decisions.

This checklist walks you through exactly what needs to be done and why it matters.

✅ The 7-Step Year-End Bookkeeping Checklist

1. Reconcile Bank and Credit Card Accounts

This is the foundation of accurate bookkeeping.

Every transaction in your accounting software should match your bank and credit card statements — line by line.

What to check:

- All deposits and withdrawals are recorded

- No duplicate or missing transactions

- No uncategorized entries left behind

Most business owners make the mistake of only reconciling the last month. That’s not enough.

👉 Go back through the entire year.

If your accounts aren’t reconciled, your financial reports are unreliable which means every decision you make based on them is a guess.

Why it matters:

Accurate books start here. Without this step, everything else falls apart.

2. Reconcile GST/HST

If you collect GST/HST, this step is critical.

You need to confirm that:

- The amount you collected matches your sales

- The amount you remitted matches CRA filings

- There are no missing or incorrectly coded transactions

Common issues include:

- Forgetting to account for GST on certain invoices

- Incorrect tax coding in software

- Filing amounts that don’t match actual records

👉 Even small discrepancies can trigger CRA attention.

Why it matters:

Proper GST reconciliation helps you avoid audits, penalties, and unexpected tax adjustments.

3. Clean Up Accounts Receivable and Payable

Now it’s time to review what’s owed — both to you and by you.

Accounts Receivable (Money owed to you)

- Identify overdue invoices

- Follow up or write off uncollectible amounts

- Remove unrealistic balances

Accounts Payable (Money you owe)

- Enter all outstanding bills

- Include December expenses (even if received in January)

- Ensure nothing is missing

👉 If this step is skipped, your income can look higher than it actually is which means you pay more tax than necessary.

Why it matters:

Clean receivables and payables ensure your financial statements reflect reality.

4. Update Your CCA Schedule (Assets & Depreciation)

If you purchased equipment, vehicles, or technology during the year, they need to be properly recorded.

This includes:

- Assigning the correct CCA class

- Adding new assets

- Removing disposed or sold assets

- Calculating depreciation correctly

Many businesses miss out on deductions simply because assets aren’t tracked properly.

👉 This is especially important for:

- Vehicles

- Equipment

- Computers and software

Why it matters:

Proper asset tracking ensures you maximize deductions and avoid errors in tax reporting.

5. Confirm Payroll Accuracy

If you have employees or contractors, payroll needs to be reviewed carefully.

Check that:

- All payroll remittances were made on time

- CPP and EI contributions are accurate

- Salaries and wages match records

- T4 and T4A slips are ready for filing

Late or incorrect payroll filings can result in:

- Penalties

- Interest charges

- CRA follow-ups

👉 This is one of the most common compliance issues for small businesses.

Why it matters:

Accurate payroll keeps you compliant and avoids unnecessary penalties.

6. Document Owner Draws and Shareholder Loans

This is where many business owners run into trouble.

If you’ve taken money out of the business, it must be recorded correctly.

For corporations:

- Withdrawals may be classified as shareholder loans

- These may need to be repaid or reported as income

For sole proprietors:

- Personal withdrawals should be clearly separated

- Business expenses should not be mixed with personal spending

👉 Poor documentation here can lead to unexpected tax consequences.

Why it matters:

Clear records protect you from tax issues and keep your books accurate.

7. Organize Receipts and Supporting Documents

Finally, make sure everything is documented and easy to access.

Gather:

- Bank and credit card statements

- Receipts and invoices

- Loan and financing documents

- CRA notices or correspondence

Best practice:

- Store everything digitally

- Organize by month

- Use cloud storage (e.g., Google Drive)

👉 CRA requires records to be kept for several years — and they must be accessible if requested.

Why it matters:

Good organization saves time, reduces stress, and protects you in case of a review.

💡 The Bottom Line

A little effort before year-end goes a long way.

When your books are clean:

- Your accountant spends less time fixing errors

- You get better tax advice

- You avoid unnecessary stress

- And most importantly — you keep more of your money

📊 Why This Checklist Matters

⏱ Save Time

Well-prepared books reduce back-and-forth and speed up your year-end process.

💰 Save Money

Accurate records ensure you claim every deduction available to you.

🛡 Reduce Risk

Stay compliant and avoid penalties, audits, or CRA issues.

📈 Make Better Decisions

Reliable numbers give you clarity and confidence to grow your business.

⚠️ Don’t Wait Until January

Waiting until the last minute creates unnecessary pressure — and often leads to mistakes.

Handling this now means:

- Less stress

- Better accuracy

- Lower costs

You’ll thank yourself later.

👉 Need Help Getting Your Books Year-End Ready?

If you’re behind or unsure where to start, we can help.

At Markham Bookkeeping, we help Edmonton small businesses clean up their books and prepare for year-end — so your accountant can focus on strategy, not fixing errors.

👉 Full breakdown here:

https://markhambookkeeping.ca/edmonton-small-business-bookkeeping-cleanup-guide/